What is Rupee Cost Averaging?

Most beginners worry about buying "at the peak" just before a market crash. Rupee Cost Averaging (RCA) is the built-in insurance policy of an SIP that solves this fear.

When you commit to a fixed amount (say ₹5,000) every month, the number of units you buy fluctuates based on the market price (NAV):

- Market is Bullish (High Prices): Your ₹5,000 buys fewer units.

- Market is Bearish (Low Prices): Your ₹5,000 buys more units.

Because you automatically buy more when prices are "on sale," your average cost per unit over a year is often lower than the average market price during that same period.

Rupee Cost Averaging: The "Volatility Experiment"

To understand why a Systematic Investment Plan (SIP) is so powerful, let’s look at a real-world mathematical scenario. Suppose you have ₹10,000 to invest over 5 months in a volatile market.

The Scenario: A "V-Shaped" Market

Imagine a stock or mutual fund where the price starts at ₹100, crashes during a mid-year correction to ₹70, and then recovers to ₹110.

The Comparison: SIP vs. Lumpsum

If you had invested the entire ₹10,000 as a Lumpsum at the very beginning (Month 1), your math would look like this:

- Total Units Owned: ₹10,000 / ₹100 = 100.00

- Final Value (Month 5): 100 x ₹110 = ₹11,000

- Average Cost per Unit: ₹100

Now, look at the SIP (Rupee Cost Averaging) result:

- Total Units Owned: 113.98

- Final Value (Month 5): 113.98 x ₹110 = ₹12,537.30

- Average Cost per Unit: ₹10,000 / 113.98 = ₹87.74

Why the SIP Won

As you can see in the chart below, while the market price fluctuated wildly, the SIP investor's average cost stayed consistently lower than the initial starting price.

- Buying the Dip: In Month 3, when the price crashed to ₹70, the SIP automatically bought 28.57 units (the highest amount in the table).

- Market Protection: Even though the final market price (₹110) is only 10% higher than the starting price (₹100), the SIP investor made a 25.3% return (₹12,537 vs ₹10,000) because they bought so many extra units while prices were low.

The Mathematical Formula

The secret to Rupee Cost Averaging is that it uses the Harmonic Mean of prices, which is always less than or equal to the Arithmetic Mean.

Average Cost = Total Amount Invested /Total Units Purchased

By keeping the "Amount" constant (₹2,000), you mathematically force yourself to buy more when the market is cheap without having to think about it.

SIP Example

The biggest mistake beginners make is waiting until they have a "large amount" to invest. In the world of wealth creation, Time is more powerful than the Amount.

Investing ₹500 today is often mathematically superior to waiting a year and investing ₹5,000. Why? Because of Compounding. When you invest early, your returns start earning their own returns.

The Math of Waiting: If you start an SIP of ₹5,000 at age 25, you could potentially retire with a much larger corpus than someone starting with ₹10,000 at age 35. You can't get back the years you lost, no matter how much you invest later.

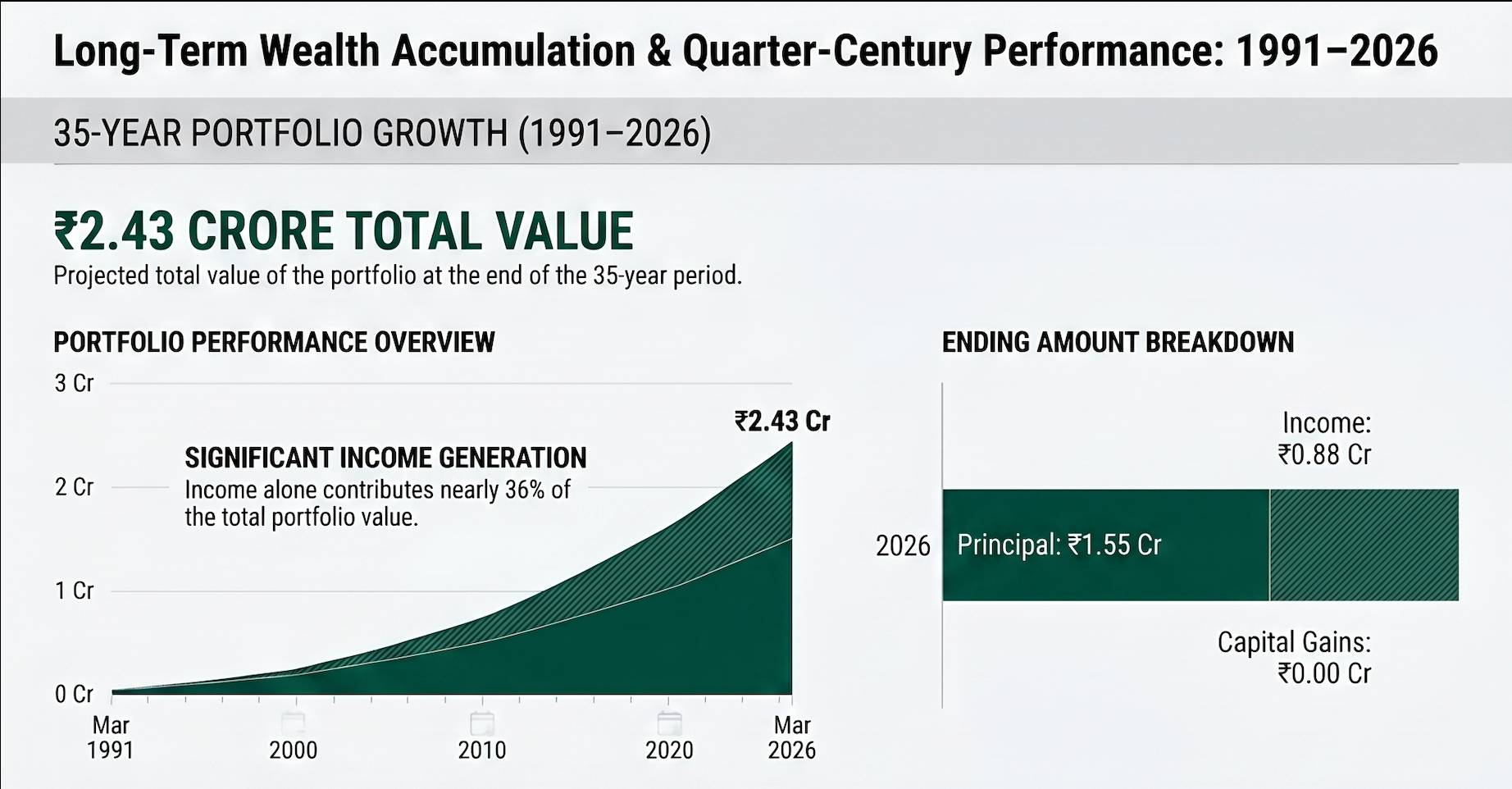

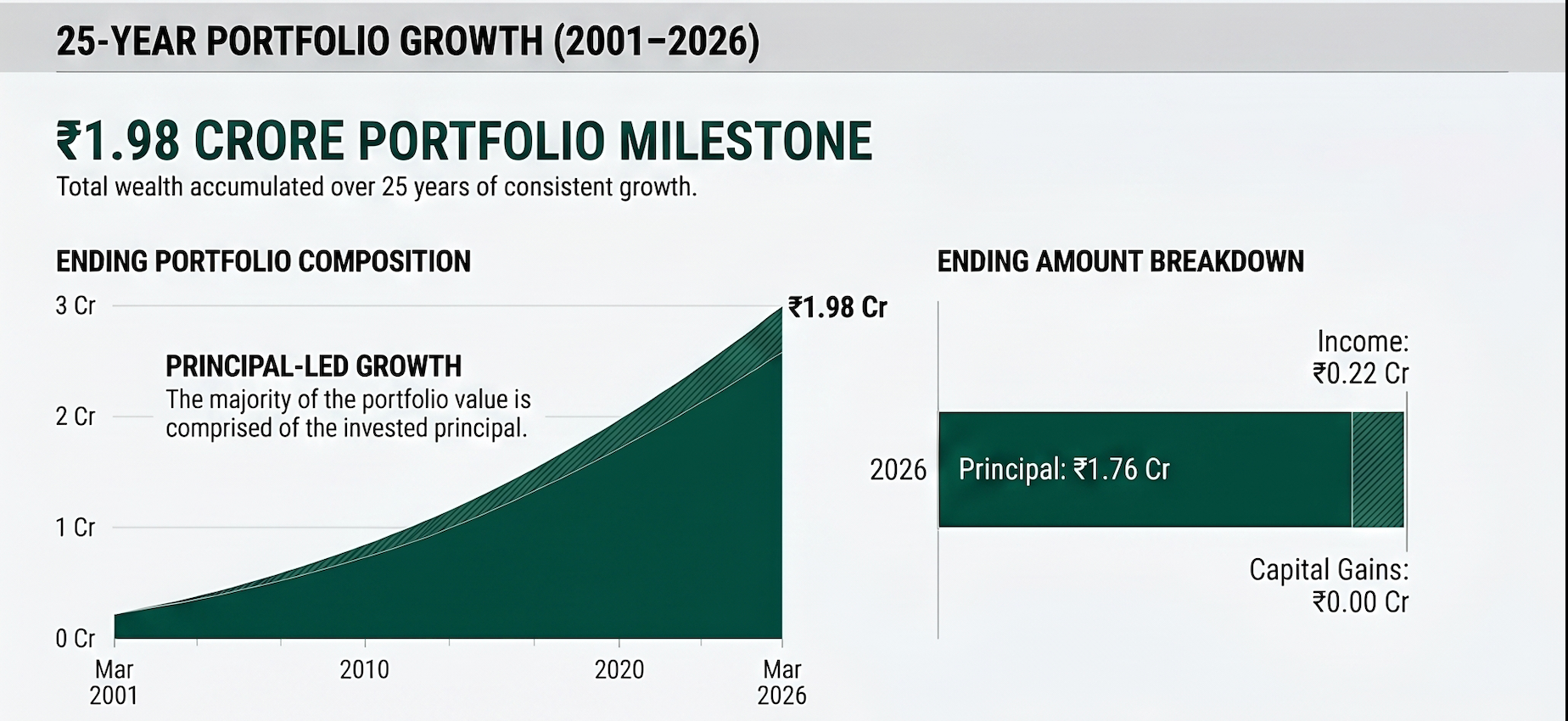

Below are two scenarios showing how a ₹5,000 SIP would have grown over 35 years (age 25 to 60) vs how a ₹10,000 SIP would have grown over 25 years (age 35 to 60) in the same fund.

Bonus! Step-Up SIP: The Wealth Accelerator

While a standard SIP is great, the Step-Up SIP is how you reach your goals faster. As your salary increases each year, you can automate your SIP to increase by a small percentage (e.g., 10% every year).

The Power of the Step-Up: from the example above, a ₹5,000 monthly SIP for 35 years yields ~ 2.43 Crore. Increasing that SIP by just 10% every year would yield ~ 7.41 Crore. A small increment, with a massive result!

.svg?v=88090ef708)